.avif)

Introduction

If you've ever scratched your head wondering why your sales reps' commission payouts seem lighter than expected, or why your payroll software insists on treating commissions differently from salaries, you're not alone.

Taxing sales commissions is one of those areas where compliance meets complexity. It's not just about calculating percentages. It's about knowing whether to apply flat or blended rates, understanding how commissions fit into payroll cycles, and making sure you're withholding correctly whether your reps are full-time employees or 1099 contractors.

Here's the good news: once you understand the structure, the rules are quite manageable.

In this guide, we'll break down how commissions are taxed in 2026, from federal and state withholding to FICA deductions and self-employment tax for contractors. You'll learn how much tax is taken from sales commissions, when to use flat versus aggregate methods, and how to stay compliant whether you're working with W-2 or 1099 reps.

Let's demystify the sales commission tax rate so you can pay accurately, stay compliant, and avoid costly surprises.

What Is the Sales Commission Tax Rate?

Sales commissions are considered taxable income by the IRS. They are typically taxed at a federal flat rate of 22% using the supplemental wage method. Additional deductions include 7.65% for Social Security and Medicare (FICA) and varying state income tax rates.

W-2 employees have taxes withheld by employers, while 1099 contractors must pay self-employment tax. The tax rate can change based on income level, state laws, and whether flat or aggregate methods are used.

Understanding these rules helps employers withhold correctly and ensures sales professionals estimate their tax obligations accurately.

As per 2026 IRS Publication 15, when commissions are paid separately or clearly identified apart from base wages, the 22% federal flat rate applies in 2026. If an employee earns over $1 million in supplemental income during the year, any amount beyond that is subject to a 37% federal withholding rate.

FICA taxes are also mandatory. Employers must withhold 6.2% for Social Security (up to the wage cap of $176,100) and 1.45% for Medicare, with an extra 0.9% Medicare tax on earnings above $200,000, as per IRS Publication 15-A.

On top of federal withholding and FICA, state income taxes may also apply. For instance, California applies a 10.23% rate for bonuses and stock options, and 6.6% for other supplemental income. In contrast, states like Texas and Florida don't impose any personal income tax.

So how much is sales commission taxed? It depends, but for most W-2 reps, the combined federal, FICA, and state rates can easily add up to 30–40% of the commission payout. We will discuss these in detail further.

To stay ahead of the latest benchmarks and trends shaping commission structures, this resource provides a comprehensive overview.

How Is Sales Commission Taxed?

Sales commissions are not taxed the same way as regular wages because the IRS classifies them differently. Commissions fall under the category of supplemental wages, which means they follow specific withholding rules that differ from standard salary payments. This classification affects how taxes are calculated and reported by employers, and how they're ultimately paid by taxpayers receiving commissions.

Below are the key distinctions and what they mean for both businesses and sales professionals.

Regular Wages vs Commission Income

Regular wages refer to a fixed salary or hourly rate. These are taxed based on the IRS's standard withholding tables, which factor in income level and filing status. Commissions, on the other hand, are treated as supplemental income, which makes their tax treatment different.

If commissions are paid in the same paycheck as regular wages and are not listed separately, they are taxed using the aggregate method. This means the employer combines the total and applies the employee's usual withholding rate. But if commissions are paid out in a separate check or clearly stated apart from regular wages, the flat supplemental rate of 22% typically applies.

This distinction influences not just how much tax is withheld but also how employers report and manage payroll.

Are Commissions Taxed Differently Than Salaries?

Yes, and it's a key distinction for both payroll teams and sales reps to understand. While base salaries follow predictable tax tables, commissions are subject to separate rules under the IRS's guidelines for supplemental income. That means withholding on commissions may be higher or lower than on salaries, depending on timing and method of payment.

This matters even more when commissions make up a large part of a rep's total income. If you're using the flat-rate method, for example, a rep might see 22% withheld federally, plus FICA and state taxes, even if their income would normally fall into a lower bracket under regular wage rules.

For employers, choosing the correct method depends on how payroll is structured. For sales reps, it affects take-home pay and how they prepare for tax season. Understanding the difference ensures accurate withholding and better financial planning.

When reps don't understand how their commissions are taxed, it can lead to mistrust and frustration. Everstage's payee experience tools let reps view their earnings, tax breakdowns, and payout history in real time. This improves transparency and builds confidence in your compensation process.

What Tax Rates Apply to Sales Commissions?

Understanding the tax rates on commissions means looking beyond just the federal flat rate. Employers must account for federal income tax, Social Security and Medicare deductions (FICA), and varying state-level rules. Each layer affects how much of a sales rep's commission ultimately reaches their pocket.

Here's a breakdown of how these rates apply across federal, FICA, and state levels.

1. Federal Tax Withholding on Commissions

The IRS treats commissions as supplemental wages, which are taxed differently than standard salary income. When commissions are paid separately or clearly designated apart from regular wages, the IRS allows employers to withhold a flat 22% federal income tax rate in 2026.

However, if an employee earns over $1 million in supplemental wages in a calendar year, any income above that threshold is taxed at a mandatory 37% withholding rate, often referred to as the high earner threshold.

If commissions are not separated out and are instead paid with regular wages, the employer may need to use the aggregate method, which calculates withholding based on the employee's total earnings and Form W-4.

Either way, the goal is to ensure accurate withholding that aligns with IRS compliance while avoiding unexpected tax bills for employees.

2. Social Security and Medicare (FICA) Deductions

In addition to federal income tax, employers must withhold FICA taxes from commission income. These cover Social Security and Medicare, and the rules are non-negotiable regardless of how the commission is paid.

According to IRS Publication 15-A:

- Social Security tax: 6.2% on total wages and commissions combined up to $176,100 annually in 2026

- Medicare tax: 1.45% on all earnings, with no cap

- Additional Medicare tax: 0.9% on wages exceeding $200,000, withheld from the employee only

Together, these add 7.65% in mandatory deductions on most commissions. The employer matches this contribution, but the employee sees their half directly withheld from each paycheck.

Because these taxes are automatic, they often get overlooked when calculating how much sales commission is taxed. But they significantly affect take-home pay, especially for high earners.

3. State Taxes on Commission Income

Beyond federal and FICA deductions, state income tax can vary widely based on where the employee works or resides. Some states apply special supplemental rates for bonuses and commissions, while others apply standard income tax rates with no distinction.

Here are a few examples of state supplemental wage tax rates based on 2026 data (source). Note: These rates apply specifically to supplemental wages like commissions and may differ from standard income tax rates:

- California: 10.23% for bonuses/stock options and 6.6% for other supplemental wages

- New York: Up to 11.7%, depending on income level and locality

- Kansas & Massachusetts: 5% flat supplemental rate

- Florida & Texas: 0% (no personal state income tax)

Employers operating in multiple states must stay updated on each jurisdiction's rules. Some states also factor local or city-level taxes into the mix. Not applying the correct state withholding rate can result in compliance issues or unpleasant surprises for employees come tax time.

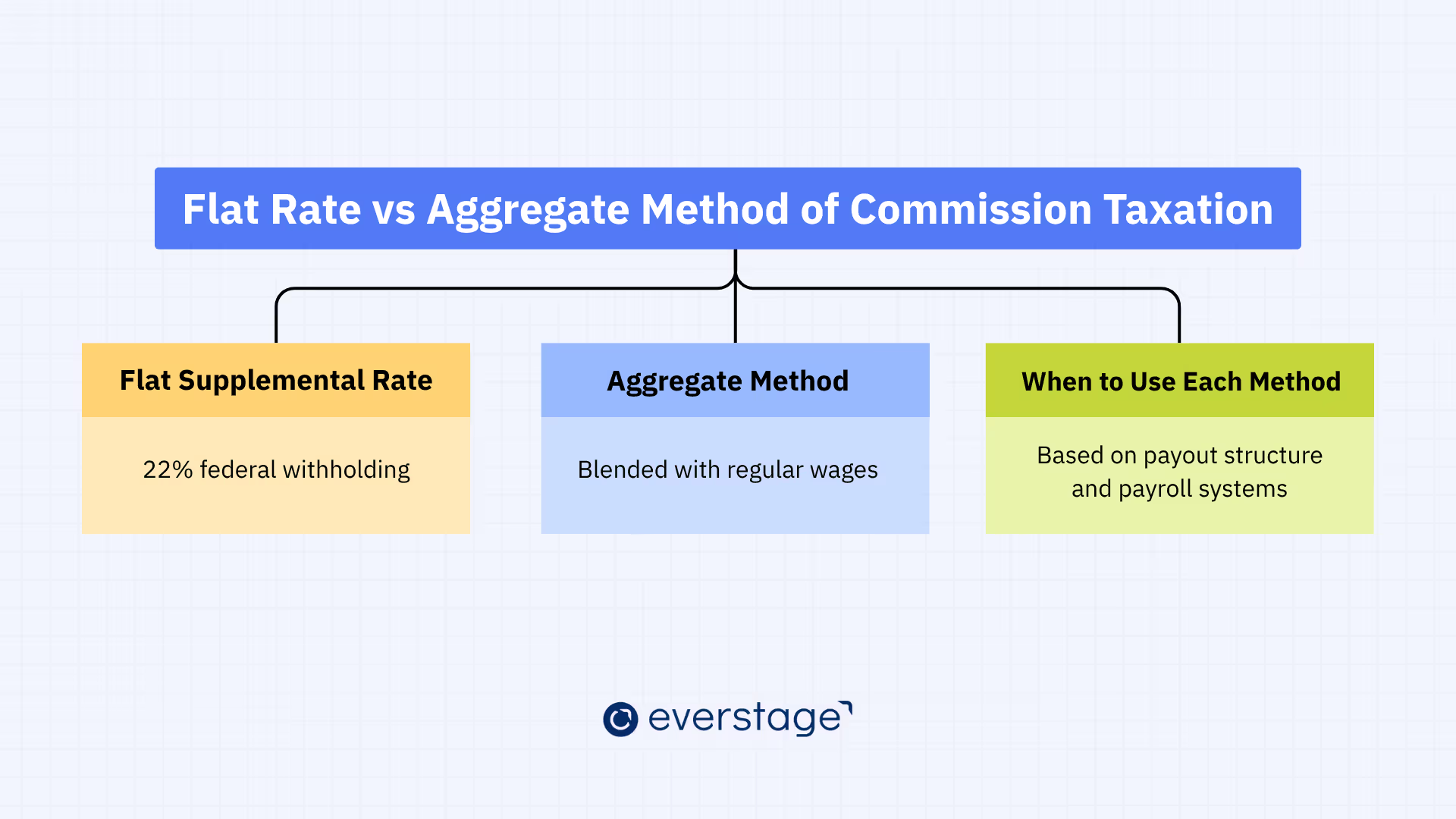

Flat Rate vs Aggregate Method of Commission Taxation

There are two main ways to withhold taxes from sales commissions: the flat supplemental rate method and the aggregate method. The choice affects how much tax is withheld and how accurate those withholdings are relative to an employee's annual tax bill. Employers must understand when each method applies and what trade-offs are involved.

Here's how both methods work and how to choose the right one for your business.

What Is the Flat Supplemental Rate?

The flat supplemental rate is a method approved by the IRS for taxing commission income that is paid separately or clearly itemized apart from regular wages. In 2026, that rate is 22% at the federal level, regardless of the employee's tax bracket.

The biggest advantage of this method is simplicity and consistency. Employers apply the 22% rate across all qualifying commission payments, avoiding the need to recalculate withholding every time.

For high earners whose total supplemental pay exceeds $1 million, the IRS mandates a 37% withholding rate for the portion over that threshold.

This method is particularly useful when commissions are large, infrequent, or separated from regular payroll cycles. It also makes it easier to forecast cash flow and build predictable processes into your payroll system.

What Is the Aggregate Method?

The aggregate method is used when commission payments are combined with regular wages in a single paycheck and are not specifically identified. In this case, the employer must calculate withholding based on the employee's W-4 form and total earnings, just as they would with a regular salary payment.

This method may result in higher or lower withholding, depending on the employee's tax situation. It can feel more accurate because it reflects the employee's actual annual tax rate. However, it is more complex to calculate and harder to automate, especially in fast-paced sales organizations with fluctuating commission cycles.

Employers using this method need payroll systems that can handle dynamic calculations and apply the correct tax tables for blended pay.

Which One Applies to Your Business?

Both methods are legal, and the method used is primarily determined by how commissions are paid, whether they are issued separately or combined with base wages, rather than by employer preference.

The flat rate is typically used when:

- Commissions are paid separately from base pay

- You want consistent withholding across reps

- Your payroll system or provider supports fixed-rate classification

The aggregate method may be better when:

- Commissions are integrated into regular pay cycles

- You want tax withholding to align with actual income brackets

- You have access to sophisticated payroll tools or custom setups

Ultimately, the method you choose should align with your commission payment schedule, payroll software capabilities, and the level of control you want over withholdings. Some businesses even use both methods in different scenarios, depending on how and when commissions are paid.

If you want to remove the manual guesswork and ensure accurate, compliant commission calculations at scale, Everstage's Sales Compensation Automation and Commission Processing platform can help. These systems automatically apply the right tax logic, manage payout rules, and integrate with your payroll, so you don't have to choose between compliance and speed.

Flat Rate vs Aggregate Method: Quick Comparison

If you're looking to align your compensation budgets with these tax considerations while planning for growth, this webinar covers strategic approaches for financial services leaders.

Commission Taxation for 1099 vs W-2 Workers (with Examples)

.avif)

Sales commissions are taxed differently depending on whether your sales reps are classified as W-2 employees or 1099 independent contractors. Each classification has its own set of tax responsibilities, reporting obligations, and payroll processing rules. Misclassifying a rep can lead to major compliance issues, so it's important to get this right.

Let's break down what each type of worker owes, and how employers should handle tax reporting.

Employee Withholding Considerations (W-2)

For W-2 employees, the employer is responsible for withholding all applicable taxes. This includes:

- Federal income tax (typically 22% if commissions are paid separately)

- FICA taxes: 6.2% Social Security and 1.45% Medicare

- Additional Medicare tax of 0.9% for earnings above $200,000

- State income tax, based on the employee's work or residence location

These taxes are withheld directly from each paycheck and reported via standard payroll filings such as Form W-2.

Employers must also contribute the matching portion of FICA taxes and ensure the payroll system is set up to identify and classify commissions properly for accurate withholding.

Example: W-2 Rep Earning Base + Commission

Suppose a sales rep earns a $60,000 base salary and an additional $40,000 in commissions in 2026.

- Federal tax on commission: 22% of $40,000 = $8,800

- FICA (employee portion): 7.65% of $100,000 = $7,650

- State tax (e.g., California at 6.6%): 6.6% of $40,000 = $2,640

In total, this rep could have over $19,000 withheld for tax obligations across federal, state, and FICA layers. Accurate classification ensures the rep isn't under-withheld and avoids surprises during tax season.

Tracking these numbers across your team can be difficult, especially when commission payouts vary every month. Everstage's reporting and analytics gives finance and RevOps leaders full visibility into earnings, tax breakdowns, and trends. This helps prevent errors and keeps everyone on the same page.

Independent Contractor Tax Responsibilities (1099)

For 1099 contractors, commissions are treated as self-employment income. Employers do not withhold any taxes. Instead, contractors are responsible for calculating and paying their own:

- Federal income tax

- Self-employment tax of 15.3%, which includes both the employer and employee shares of Social Security and Medicare

- State income taxes, depending on where they operate

- Quarterly estimated tax payments via Form 1040-ES

Employers must issue a Form 1099-NEC, which applies specifically to non-employee compensation such as commissions, for any contractor paid more than $600 during the year, reporting the full commission amount without deductions. Other types of payments to contractors may require different 1099 forms depending on the nature of the transaction.

Example: 1099 Contractor on Commission

Let's say a contractor earns $100,000 in total commissions in 2026.

- Self-employment tax: 15.3% of $100,000 = $15,300

- Federal income tax: Based on their tax bracket

- State income tax: Varies by state (e.g., none in Texas, 6% in Iowa)

Since no taxes are withheld by the company, the contractor must pay directly to the IRS every quarter. Failing to do so may result in interest charges or penalties.

To put these commission structures into practice, having a clear agreement in place helps prevent disputes and ensures all parties understand the terms upfront.

Conclusion

Commission payouts can be a powerful motivator, but only if they're handled right. From flat versus aggregate methods to federal, FICA, and state taxes, understanding how commissions are taxed is crucial for both compliance and trust. Whether you're paying W-2 reps or 1099 contractors, getting it wrong can lead to under-withholding, tax penalties, or frustrated employees.

Once you understand the rules, it's easier to design a compensation structure that keeps your team happy and your business compliant. That means choosing the right tax method, using smart payroll systems, and staying on top of ever-changing state rates.

At Everstage, we help sales and RevOps leaders simplify commission planning, payouts, and tax reporting with full transparency and automation. If you're looking to improve compliance and give your reps clearer visibility into their earnings, our platform can help.

Book a free consultation with Everstage to make your commission workflows smarter and stress-free.

Frequently Asked Questions

What is the tax rate on sales commissions?

Sales commissions are taxed as supplemental income. In 2026, the IRS applies a flat federal withholding rate of 22% for most commissions. Additional deductions include 7.65% for FICA (Social Security and Medicare) and applicable state income tax, which varies by location.

Are sales commissions taxed differently than regular salary?

Yes. Sales commissions are classified as supplemental wages by the IRS and may be taxed using either the flat rate method or the aggregate method, depending on how they are paid and employer discretion. Regular salaries follow standard income tax withholding tables.

How do I calculate taxes on sales commission income?

To calculate taxes on commission, apply the 22% federal supplemental rate, add FICA taxes (7.65%), and include state-specific income tax rates. You can also automate the entire process with a platform like Everstage, which applies the right tax logic, handles edge cases, and simplifies compliance at scale.

Are there different tax rules for 1099 vs W-2 sales commissions?

Yes. W-2 employees have income tax and FICA withheld by the employer. 1099 contractors are responsible for paying their own taxes, including 15.3% self-employment tax, and must file quarterly estimated payments. Employers must issue a 1099-NEC for commission payouts to contractors.

Why is my commission taxed more than my base pay?

Commissions may appear taxed more because of the flat supplemental withholding rate (22%) applied by default. This rate may be higher than the blended rate on your regular salary, but actual annual tax liability is reconciled at year-end when filing your tax return.

Has the sales commission tax rate changed in 2026?

The federal supplemental withholding rate remains at 22% in 2026 for commissions under $1 million. High earners above that threshold are subject to a 37% rate. Several states, including California and New York, also updated their income tax guidance for variable income.

.avif)

.avif)

.avif)

.avif)