The right retail commission structure matches your margin reality, your customer experience, and how your stores actually sell.

- Align to goals: Drive the behaviors you need, conversion, AOV, margin mix, or CX, then work backward to mechanics.

- Keep it simple: Fewer rates, clear tiers, clean rules for returns and omnichannel crediting.

- Pay on what you keep: Net of returns, discounts, and cost where margin matters.

- Test before launch: Simulate 12 months of data to find cost surprises and edge cases.

Iterate, don't ossify: Retail is seasonal; your plan should adapt with it.

You're managing thin margins, seasonality, turnover that can top 60% annually and omnichannel complexity that didn't exist a decade ago. No single commission plan will magically fix all of that. But a poorly designed one will make every problem worse.

Should you pay on sales, profit, units, or team outcomes? What happens when someone helps a customer in-store, but they finish the purchase via BOPIS? Who gets credit for a sale that gets returned three weeks later?

These are questions that finance teams face every other week.

Let's define what a retail commission structure actually is, walk through the models that work, cover design steps, and flag the traps we've seen teams fall into.

What is a Retail Commission Structure?

A retail commission structure is how you pay store associates variable compensation for selling. It defines what counts as sales, how much someone earns from those sales, plus the payout timing.

That sounds straightforward, but retail adds wrinkles absent from a typical B2B comp plan.

Sales cycles are measured in minutes. Return rates run around 16-17% of annual sales, per the National Retail Federation's 2024 Consumer Returns report, with online purchases closer to 20%. Discounting is constant. And the question of who sold it gets murky fast when one associate helps a customer, another rings them up, and a third processes the BOPIS pickup.

Then there is the omnichannel layer: ship-from-store, clienteling apps, assisted digital sales. Your commission structure has to account for all of it, or your floor team will start treating your own ecommerce channel as the competition.

Salesforce research shows that unrealistic sales targets are the top reason reps leave a job, followed closely by uncompetitive pay. In retail, comp clarity is harder to achieve because return, credit, and discount logic add layers that most comp plans were never built to handle.

As Sucharita Kodali, VP and Principal Analyst at Forrester, has noted, the way retailers structure incentives directly shapes the customer experience. Associates incentivized to push high-margin products that customers do not need erode trust. Associates rewarded for solving problems and building baskets thoughtfully drive both revenue and loyalty.

That tension between margin protection and customer experience is the central design challenge of any retail commission structure.

Every plan has a few core building blocks:

- Earning basis: What sales count toward commission from gross sales, net sales, or gross margin dollars.

- Rates and tiers: The percentage or dollar amount earned, plus whether rates increase as performance climbs.

- Credit rules: Who gets paid on which transaction, including assisted or shared-credit scenarios.

- Clawback window: How long after a sale returns can a payout be reduced.

- Payout cadence: Weekly, biweekly, or monthly, and whether true-ups apply.

When these pieces are well-designed and communicated clearly, associates can connect their daily activity to their earnings in real time. When they are not, you get confusion, disputes, and associates who game whatever part of the plan they can decode.

Why a Thoughtful Retail Commission Structure Matters

In retail, where frontline associates are your brand in the customer's eyes, getting comp right is a revenue lever, not a back-office exercise.

- Drive the right behaviors:A well-designed plan pushes conversion, stronger average order value, and better attachment performance. Pay only on top-line revenue, and you will get associates who chase the easiest sale and skip the accessory conversation.

- Protect margin: Paying on gross profit rather than gross sales discourages discount-first selling. In practice, this single shift changes floor behavior faster than most training programs. Forrester has flagged promotional leakage, unplanned margin loss from excessive or poorly targeted discounting, as a persistent problem for retailers whose incentives have no connection to profitability.

- Retain top talent: Clear, fair pay reduces churn. Associates who understand exactly how they earn and trust that payouts are accurate stay longer. In a sector where replacing a single associate can cost thousands in recruiting and ramp time, comp clarity is a retention infrastructure.

- Align omnichannel: Store teams that receive no credit for BOPIS orders or assisted digital sales will steer customers away from your own online channel. Rick Watson, founder of RMW Commerce Consulting, has argued that channel conflict in retail almost always traces back to misaligned incentives. Credit the behavior you want, and the channel friction eases.

- Reduce pay disputes: Clear payout rules significantly cut payroll headaches, especially around returns and credit disputes. Gartner's sales performance management research emphasizes that auditability and transparent crediting rules are foundational to any comp program that associates and finance can both trust.

Types of Retail Commission Models

There is no universal model. The right one depends on your selling motion, margin profile, plus the behavior you want to drive.

1. Differential and Category Rates

You pay a higher commission percentage on strategic categories or attachments, cases, extended warranties and premium product lines, while keeping a standard rate on everything else.

Best for: Retailers focused on attach rates or pushing specific product families. Think phone cases alongside device sales, or styling products alongside salon services.

Watch out: The temptation is to create a different rate for every department. Past two or three priority rates, associates cannot keep the math straight and stop trying. Pick your priorities for the season, communicate them clearly, and rotate as the business shifts.

2. SPIFFs

A per-item or per-goal bonus for selling specific SKUs or completing targeted behaviors. Ten dollars for every unit of a new product sold during launch week is a classic example.

Best for: Vendor-funded pushes, seasonal campaigns, or when you need a short burst of focus on a particular item or behavior. SPIFFs work because they are immediate and easy to understand.

Watch out: SPIFFs should layer on top of your core plan. If associates start ignoring their base commission to chase SPIFFs, the plan has a design problem. Track vendor funding carefully and audit payouts; loose SPIFF management is one of the fastest ways to leak margin.

3. Team and Store Pool

A bonus pool funded by total store performance, usually a percentage of store revenue or margin, is split among associates by hours worked or individual contribution.

Best for: High-collaboration floors where handoffs happen constantly. If your selling model involves one person greeting, another fitting, and a third closing at the register, individual commission creates conflict. A team pool rewards the outcome that everyone contributed to.

Watch out: Pure team pools can demotivate your top performers. Add a light individual kicker so outsized effort gets recognized. Your best sellers will otherwise subsidize everyone else and eventually leave.

4. Quota Plus Accelerators

Each associate has a monthly or weekly sales target. They earn a base rate up to quota and a higher accelerator rate on everything above it.

Best for: High-ticket consultative retail like kitchens, appliances, and furniture, where each sale takes real effort and expertise.

Watch out: Set quotas relative to store traffic, not just historical averages. A location with half the foot traffic should carry a proportionally smaller target. A flat annual quota in a business with a massive Q4 spike will underpay in December and overpay in March.

5. Draw Against Commission

An advance paid against future commissions. In a recoverable draw, the associate owes back the difference if commissions fall short. In a non-recoverable draw, the advance is a guaranteed floor.

Best for: New store openings, ramping new hires, or high-ticket environments where early months are slow while associates build a client book.

Watch out: Draw legality and recovery rules vary by state and country. Some jurisdictions restrict recoverable draws entirely. Document everything in your plan, and involve HR and legal counsel before implementation.

6. Hybrid Omnichannel Crediting

Associates receive credit for assisted digital orders, appointments booked in-store that convert online, live chat interactions, or BOPIS upsells at pickup.

Best for: Omnichannel retailers where store staff meaningfully influence online revenue. If an associate spends 20 minutes with a customer who then buys from the app in the parking lot, your comp plan should acknowledge that.

Watch out: You need clear rules for evidence and time windows. Define what counts as assisted: an appointment ID, a clienteling app log, a chat transcript. Set a credit window, seven days from the last interaction is common, and stick to it. Loose definitions lead to double payments or a backlog of disputes.

Quick-Fit Guide by Retail Format

Retail commission model recommendations by store format

This is a starting point, not a prescription. Your format, margins, and selling motion should drive the final choice.

How to Calculate Retail Commissions: Worked Examples

Here are three calculations showing how common retail commission models play out in practice, including the return and discount handling that most examples skip.

Example A: Tiered Percent on Net Sales

An associate sells $28,000 gross in a month. Returns within the 30-day window total $2,400, bringing net sales to $25,600.

Rates: 2% on the first $20,000; 3% on everything above.

- First $20,000 × 2% = $400

- Remaining $5,600 × 3% = $168

- Total payout: $568

Without the return clawback, the payout would have been $640. That $72 difference is exactly why paying on net matters for margin control.

Example B: Gross Margin Model

An associate sells a product for $5,000. COGS is $3,500, and the applied discount is $300.

Gross margin: $5,000 − $3,500 − $300 = $1,200

Rate: 10% of margin dollars. Payout: $1,200 × 10% = $120

The catch: Margin models only work when COGS data is timely and accurate. If cost feeds lag by a month, you are either holding paychecks or truing up retroactively, and neither builds trust.

Example C: Attach-Rate SPIFF Plus Team Pool

An associate earns a $5 SPIFF per warranty sold and moves 18 warranties in the month. The store hits its monthly revenue target, triggering a team pool that pays this associate a $150 share based on hours worked.

- 18 warranties × $5 = $90 SPIFF payout

- Team pool share = $150

- Total variable payout: $240 on top of base or hourly pay

This combination rewards individual hustle through the SPIFF and collective store performance through the pool, which is the point when your selling model depends on handoffs and teamwork.

How to Design Your Retail Commission Structure (Step-by-Step)

Picking a model is the easy part. The hard part is wiring it to your actual business so it drives the outcomes you need without breaking payroll. Here's how to build it from the ground up.

Step 1: Set the Outcomes You Will Pay For

Pick two or three primary KPIs: conversion rate, AOV, margin mix, attachment rate, or NPS/CSAT. Weight them by season. During heavy promo weeks, lean harder on margin mix to prevent discount-first selling. During launch periods, attachment rate may matter most.

Zeynep Ton, Professor of the Practice in Operations Management at MIT Sloan and author of The Good Jobs Strategy, argues that what you measure and reward must match how the job actually works — not simply what is easiest to track.

Step 2: Choose the Earning Basis

Net sales is simple and transparent, while gross margin dollars better protect profitability. Units can make sense for high-volume categories. Blended covers multiple priorities: for example, 2% of net sales plus $3 per warranty sold.

Match the earning basis to the behaviors you are paying for. If margin matters, pay on margin.

Step 3: Set Rates, Tiers, and Accelerators

Keep tiers minimal, two or three at most. and use smooth accelerators rather than hard cliffs.

Example: 2% on the first $20,000 in net sales, 2.5% from $20,001 to $30,000, 3% above $30,000.

A hard cliff where an associate earns 2% on $19,999 but 3% on $20,001 produces sandbagging every period. Smooth accelerators remove that incentive.

Step 4: Define Omnichannel Credit Rules

Spell out who gets credit for non-traditional sales, including BOPIS and appointment-driven purchases. Require documented evidence, such as appointment IDs or client activity logs.

Avoid double-paying store and ecommerce on the same transaction unless a team pool overlay is part of the design.

Step 5: Handle Returns, Cancellations, and Discounts

Pay on net sales, after returns and discounts. Set a clear clawback window; 30 days is standard. For partial returns, claw back only the returned portion.

State your discount handling in plain language: a 20%-off promo typically reduces the commissionable base. Write it down so nobody is surprised.

Step 6: Manage Split Credit and Assisted Selling

When two associates touch the same sale, keep the rules simple: 50/50 splits by default, with documented manager override for exceptions.

Complex attribution models sound smart in a meeting but collapse on the floor.

Step 7: Normalize for Traffic and Hours

A full-timer working peak Saturday shifts should not be benchmarked against a part-timer who works Tuesday mornings. Index targets by hours worked or foot traffic. For team pools, sales per hour are more equitable than raw totals.

Step 8: Keep It Legal and Compliant

Associates on hourly-plus-commission pay who work overtime require correct regular rate calculations, a common audit flag. Draw recovery rules vary by jurisdiction. Involve HR and legal counsel before finalizing plan terms.

Nothing here constitutes legal advice.

Step 9: Communicate Simply

If the plan does not fit on one page with examples, it is too complicated. Build a summary showing how a sample paycheck breaks down. Train managers before launch; they will field most questions. Host a Q&A session before rollout.

Salesforce research consistently finds that compensation clarity is one of the strongest levers for seller engagement. In retail, where associates are often younger, less tenured, and working multiple jobs, clarity matters even more.

Step 10: Test, Simulate, and Pilot

Before going live, backtest 12 months of POS data against the new plan and check:

- Total cost to the business: Does it stay inside your comp-to-revenue envelope?

- Top versus bottom earner payouts: Are the gaps motivating or demoralizing?

- Edge cases: What happens in a month with 40% returns?

- Seasonal cost swings: Will December blow the budget?

Pilot in two or three stores first. Gather floor feedback. Iterate. Then roll out.

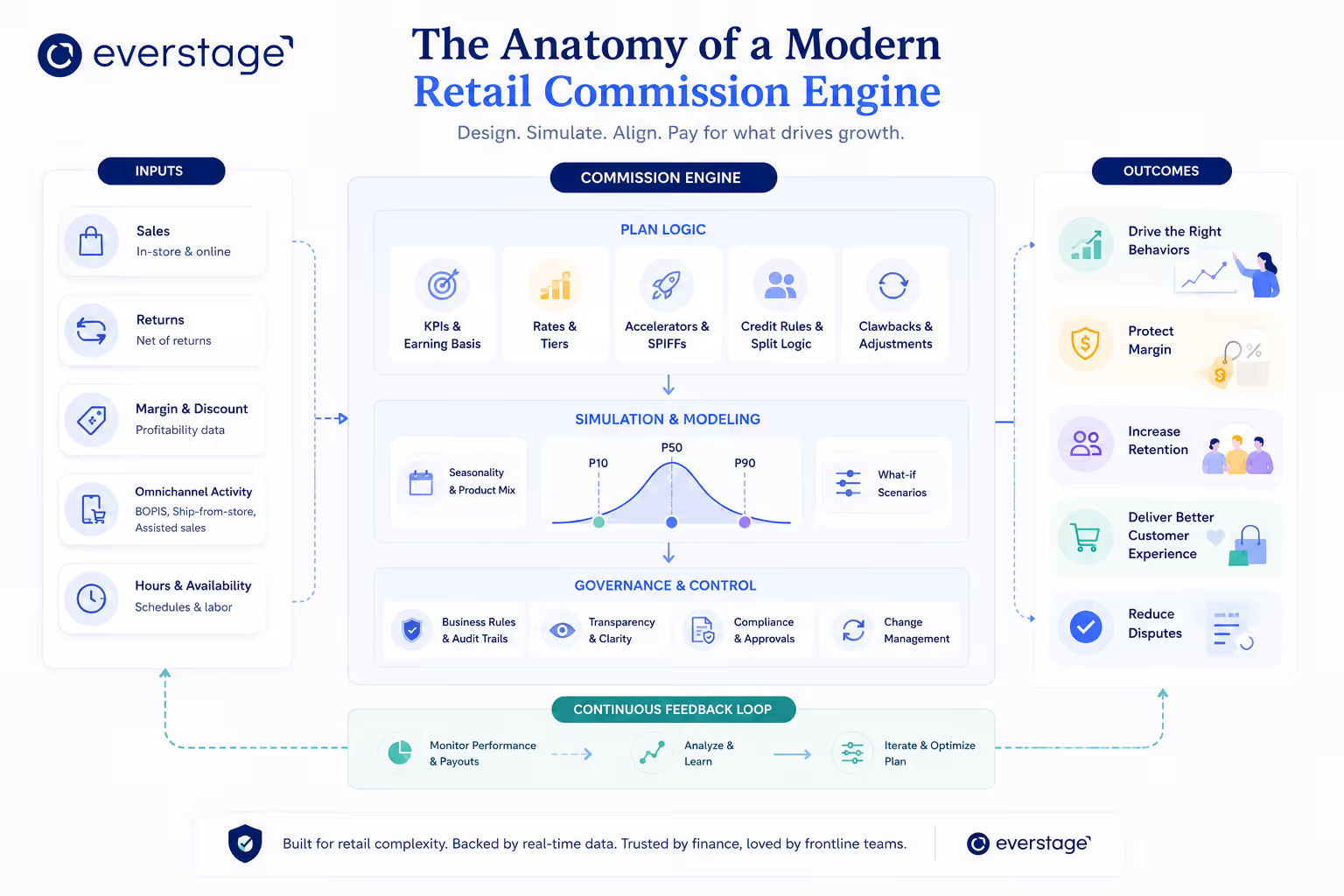

We use Everstage to simulate plan changes against POS data so teams can see cost, edge cases, and return/clawback impacts before anything hits a paycheck, along with full audit trails and version control.

Common Pitfalls and How to Fix Them

Every retail commission structure looks clean on a whiteboard. The problems surface when real-world messiness like returns, promos and shift handoffs affects the plan.

1. Overpaying on Discounts

Paying commission on the pre-discount price gives associates zero reason to protect margin during promos.

Fix: Pay on net sales or gross margin. For heavily promoted items, set a lower commission rate or cap commissionable volume.

2. Ignoring Returns

Returns that do not reduce the commissionable base become free money for associates and a margin leak for the business.

Fix: Define a clawback window (30 days is standard), reverse commission on the next pay period, and show pending clawbacks on every statement so adjustments are visible and expected.

3. Channel Conflict

Store teams with no credit for assisted digital sales will steer customers away from your own ecommerce channel.

Fix: Credit-assisted digital with clear evidence requirements (appointment IDs, chat logs) and add a small team pool tied to omnichannel KPIs like BOPIS conversion.

4. Tier Cliffs

Hard jumps between commission tiers cause end-of-period sandbagging. Associates hold orders until they cross a threshold.

Fix: Use smooth accelerators, plus 0.5% per tier, or weekly pro-ration to remove the incentive to time transactions.

5. Too Many Category Rates

Past three different rates, associates cannot do the mental math.

Fix: limit priority rates to two or three and rotate them seasonally as business priorities shift.

6. No Transparency

When an associate cannot explain how their last paycheck was calculated, the plan has failed.

Fix: Publish a plain-language plan document with example paycheck math and train managers to walk through it.

7. One-size-fits-all Quotas

A store with half the foot traffic should not carry the same quota as your flagship.

Fix: Index targets by traffic data or hours worked and revisit them each season.

8. Spreadsheet Breakage

Manual spreadsheets lack audit trails, version control, and approval workflows. Errors compound silently until a paycheck is wrong.

Fix: Move to a governed sales performance management platform with centralized rules and exception logging. Teams that centralize credit rules and return logic in Everstage see a significant drop in disputes because every adjustment is tracked and auditable.

Suggested read: How to Effectively Communicate Compensation Plan Changes to Your Sales Teams

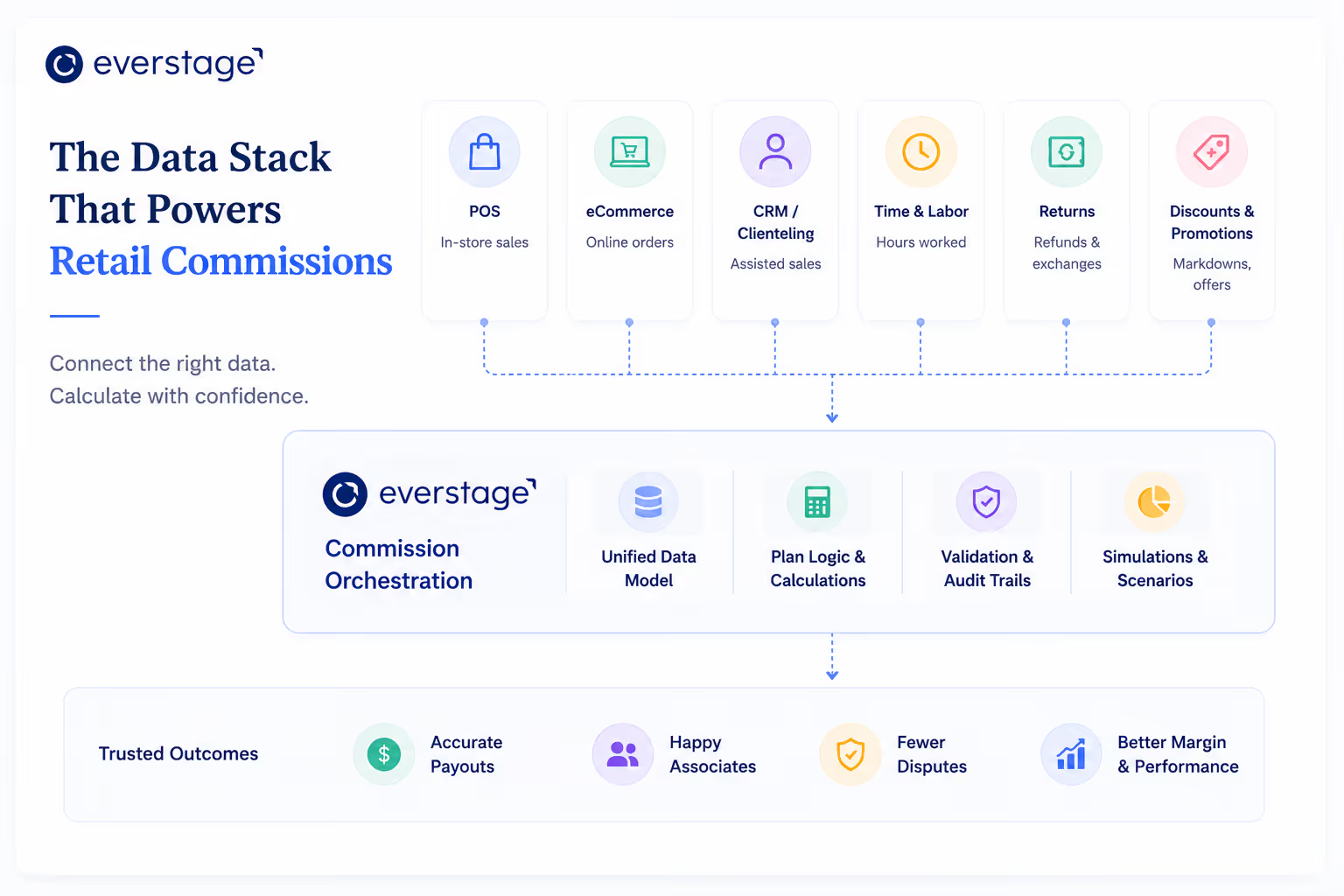

Tech and Data You Will Need to Make This Work

Your commission structure is only as good as the data feeding it. Before launch, confirm these pieces are in place.

Data Stack Checklist

- POS system with seller ID capture on every transaction, a returns feed, and discount flags

- SKU-level COGS for margin-based models, plus vendor SPIFF funding data if you run vendor-funded incentives

- Ecommerce, appointment, and clienteling data for assisted digital credit: appointment IDs, chat transcripts, client book entries

- Time and attendance for hours-based normalization and fair quota indexing

- HRIS and payroll integration with audit logs for manual adjustments and overrides

Validation Steps

Reconcile every plan rule to a data field. If the plan says pay on net sales after returns, confirm your POS passes net amounts, or that your returns feed is timely enough to calculate them.

Run exception reports for negative commissions, extreme splits, and payouts outside expected ranges. These are your early-warning system for bad data or miswritten rules.

Gartner's sales performance management research consistently treats result validation, accuracy, and auditability as foundational requirements for comp programs that scale without disputes.

Simple Plans Outperform Clever Ones

You do not need an exotic commission structure. You need one that pays for what you actually value and is simple enough to explain at a pre-shift huddle.

Complexity is usually a symptom. When a plan tries to account for every edge case, reward every behavior, and protect every margin scenario upfront, associates end up optimizing for whatever feels safest and not what the business needs.

Start with outcomes. Keep the mechanics tight. Test against real data before a single dollar hits a paycheck.

Retail changes weekly: new promos, seasonal swings, shifting channel mix. Your commission structure should evolve with it, without surprising payroll costs or breaking associate trust.

Start here: write down the top two or three behaviors you want your floor team to repeat. If a measure in your plan does not directly drive one of them, cut it.

Want to pressure-test your retail commission structure against last year's POS data and return patterns?

Book a demo to see how your team can model scenarios, automate payouts, and reduce disputes with Everstage.

Frequently Asked Questions

What is a Retail Commission Structure?

A retail commission structure is how you pay store associates variable compensation for selling. It defines what sales count toward commission, how much someone earns on those sales, and when they get paid, including rules for returns, discounts, splits, and omnichannel crediting.

What is a Good Commission Rate for Retail Associates?

It depends on your margins and return rates. In our experience, 1 to 3% of net sales is common in mid-margin categories like apparel and beauty; 5 to 10% of gross margin dollars is typical in high-ticket categories like jewelry and electronics; and store pools generally run 1 to 2% of total store sales. The best approach: start with your affordable total comp target and work backward to rates using last year's POS data.

Should Retail Pay Commission on Gross Sales or Profit?

If discounting and COGS vary significantly by SKU, profit-based pay better protects margin. If your margins are stable and returns are low, sales-based pay is simpler to explain on the floor. Many retailers blend both: a sales-based rate for the core plan plus SPIFFs on high-margin strategic attachments.

How do Returns Affect Retail Commissions?

Most retailers pay on net sales with a defined clawback window, typically 30 days. When a return falls within the window, the commission is reversed on the next paycheck. For partial returns, only the returned portion is clawed back.

How do I Handle Online Orders In-store Commission?

Credit associates for clearly assisting digital sales: appointments booked in-store that convert online, clienteling outreach, or BOPIS upsells at pickup. Require evidence (appointment IDs, chat handoffs) and set time-bound credit windows. To prevent double-paying, either split credit with ecommerce or use a small omnichannel team pool tied to BOPIS conversion and pickup experience.

Is a Draw Against Commission Legal in Retail?

In many jurisdictions, yes, but rules vary. Some states restrict recoverable draws or require specific disclosure language. Always document draw terms in your plan, and consult your HR and legal teams to comply with wage-and-hour laws, especially regarding overtime calculations for hourly-plus-commission staff. Nothing here constitutes legal advice.

More on mechanics in our Draw Against Commission glossary.

.avif)

.avif)

.avif)