Sales commission classification is crucial for accurate financial reporting, ensuring expenses align with true business performance and profitability.

- Avoid profit margin distortion by correctly categorizing commissions as period costs, not product costs.

- Improve budgeting and cash flow management with clear expense recognition.

- Leverage commission automation tools to streamline tracking and reporting.

- Enable informed decision-making by understanding the impact of commission costs on SG&A and operating expenses.

In business, knowing what goes where on the balance sheet or income statement is key to accuracy.

Whether a fixed-rate or single-rate—sales commissions often get tied to performance. They typically line up in the category of Selling, General, and Administrative expenses (SG&A) or operating expenses.

Having said that—what is the cost of sales? How do sales commissions influence your overall cost structure?

Considering how 79% of sales leaders reported revenue increases in the past year—understanding how to categorize costs is more important than ever.

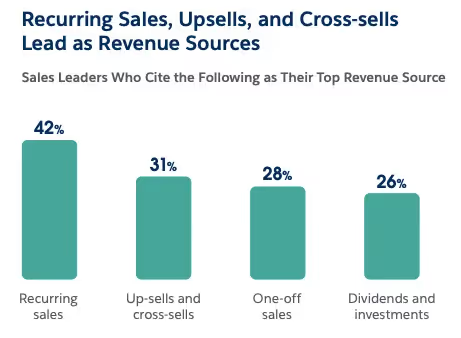

Moreover, 90% of sales teams use multiple revenue sources, of which recurring sales, upsells, and cross-sells top the list.

With all these factors adding up—making an accurate cost classification of sales commissions is vital to accurately assessing profitability.

If a sales commission is misclassified as a product cost instead of a period cost, it can inflate profit margins and distort how costs are allocated over time. For example, a company generates $500,000 in revenue and pays $100,000 as commissions to its sales reps.

By incorrectly classifying sales commissions as product costs, the company ends up spreading this expense across its inventory rather than recognizing it immediately. This could result in a higher gross profit, showing a margin of let’s say 30% instead of the correct 10%. Over time, this misrepresentation can lead stakeholders to believe the company is operating more efficiently than it is.

But what are period and product costs?

Period costs are expenses that are not directly tied to production, such as administrative and selling expenses. In contrast, product costs are directly associated with the manufacturing of goods and include direct materials and labor.

So under which bracket does sales commission fall? How do you even understand if it is a period or product cost? In this article, we will break down period and product costs, discussing how sales commissions fit into this framework. Let’s get right to it!

Period costs and product costs: What are they?

Let’s break down period and product costs to see how they influence the income statement and balance sheet.

What are period costs?

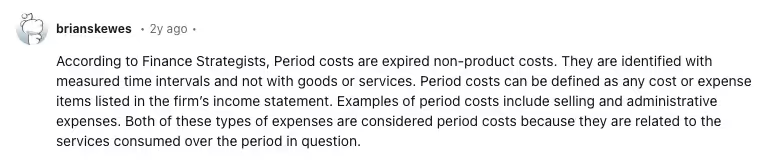

Period costs are expenses that do not directly relate to the manufacturing of goods or services. These indirect costs are incurred over a specific accounting period and are recognized on the income statement when incurred. Unlike product costs, period costs are not tied to production levels or finished goods and can impact profitability regardless of sales volume.

Types of period costs:

- Administrative expenses

- Selling expenses

- Marketing costs

- Depreciation expenses

Key characteristics of period costs

- Non-manufacturing: Period costs are associated with activities outside the production process and do not contribute to finished goods.

- Fixed and variable nature: These costs can be fixed, remaining constant regardless of production, or variable, fluctuating with business activities.

- Immediate impact on financial statements: Period costs directly affect the income statement and net income without altering the Cost of Goods Sold (COGS).

- Influence on budgeting: These costs play a crucial role in budgeting and forecasting, as they often represent ongoing operational expenses that need to be managed.

- Strategic importance: Understanding period costs helps in decision-making regarding resource allocation and evaluating the efficiency of non-manufacturing activities.

Examples of period costs

Common examples of period costs include:

- Salaries of administrative staff: Wages paid to employees who do not participate in production, such as HR and finance teams.

- Sales commissions: Payments made to sales personnel based on their sales performance, reflecting a variable cost as they depend on sales volume.

- Advertising expenses: Costs incurred for marketing campaigns aimed at promoting products, which do not tie to production levels.

- Office rent: Costs associated with leasing office space for non-production activities.

- Depreciation expense: The allocation of the cost of non-manufacturing assets over time, impacting financial reporting.

- Utilities for administrative offices: Costs for electricity and water used in non-production areas, treated as fixed or variable based on the usage.

What are product costs?

Product costs are expenses that are directly associated with the manufacturing or acquisition of goods. These costs are incurred during the production process and are included in the COGS until the products are sold. Unlike period costs, product costs are linked to production levels and can impact gross profit calculations.

Types of product costs

- Direct materials

- Direct labor

- Manufacturing overhead

Key characteristics of product costs

- Production association: Product costs are directly related to the manufacturing process and influence gross profit.

- Inventoriable costs: These costs are recorded as inventory on the balance sheet until sold, at which point they transfer to COGS.

- Direct traceability: Many product costs can be directly traced to specific products, such as direct materials and direct labor, facilitating accurate cost accounting.

- Inclusion in financial statements: Product costs are included in financial reporting as part of inventory until the products are sold, affecting both the balance sheet and income statement.

- Link to production efficiency: Analyzing product costs can reveal insights into production efficiency and overhead management, guiding operational improvements.

Examples of product costs

Product costs are expenses included in the cost of goods sold until the products are sold. These could include:

- Direct materials: Raw materials used in manufacturing, such as steel for machinery or fabric for clothing.

- Direct labor: Wages paid to workers directly involved in the production process, such as assembly line employees.

- Manufacturing overhead: Costs necessary for production but not directly tied to a specific product, such as maintenance costs for production equipment.

- Indirect materials: Supplies that support the manufacturing process but cannot be traced directly to a specific product, like cleaning supplies for the factory.

- Indirect labor: Salaries for employees who assist in production but do not directly work in manufacturing, such as supervisors or maintenance workers.

Understanding salaries as costs

Salaries can be categorized as product costs when they are associated with production staff. For example—wages for machine operators are considered product costs. On the flip side, salaries for staff who do not engage in production, such as marketing, sales, or administrative employees, are classified as period costs.

Sales commissions: A quick overview

To assess whether sales commissions are categorized as period or product costs, let’s take a moment and look at what sales commissions are.

What is a sales commission?

Sales commissions are performance-based payments made to salespeople based on their sales achievements. They serve as an incentive to drive higher sales and motivate the sales team to meet or exceed targets. Sales commissions are often a key part of a salesperson's total compensation.

Let's say Dan is a sales representative earning a base salary of $40,000. In addition, he earns a 10% commission on all sales he generates throughout the year. If Dan's total sales for the year amount to $300,000, he would earn an additional $30,000 in commissions.

Characteristics of sales commissions

- Performance-based: Commissions are tied directly to sales performance, encouraging employees to maximize sales.

- Variable compensation: Unlike fixed salaries, sales commissions fluctuate based on individual or team performance.

- Revenue-driven: Payments are often based on revenue generated, aligning employee incentives with company goals.

Common structures of sales commissions

- Fixed percentage: A basic model where salespeople earn a consistent percentage on each sale.

- Tiered commissions: Commissions increase as sales targets are met or exceeded, encouraging higher performance.

- Revenue-based: Commissions are calculated as a percentage of the revenue a salesperson brings in, often with different rates for different products or services.

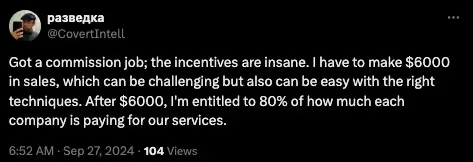

Sales commissions play a vital role in aligning the sales force with the company’s revenue goals while keeping compensation flexible and performance-driven. As this X user points out, commissions can offer significant rewards.

Should sales commissions be considered a period cost?

Sales commissions are generally considered period costs or indirect costs due to their direct link to sales performance rather than the production of goods.

Below, we will explain the criteria for determining period costs.

Criteria for determining period costs

Period costs include all expenses tied to a specific accounting period that are unrelated to manufacturing or production and are not counted as part of inventory costs.

Why it's essential to view sales commissions as period costs

Sales commissions are based on sales activity, and since they are unrelated to production, they meet the criteria for period costs. Here's a deeper look into why they fit this classification.

Financial reporting implications

- Impact on financial statements: Sales commissions are recorded as selling expenses in the income statement. They do not inflate inventory values on the balance sheet, ensuring a clear financial position. When commissions are paid, they either reduce cash flow or show up as liabilities until settled—impacting working capital.

- Accurate classification for transparency: Correctly categorizing sales commissions as period costs ensures that profit margins and financial statements are not skewed. Misclassification could lead to misleading financials and potential regulatory issues. For instance, reporting commissions as product costs would overstate inventory and gross profit, providing an inaccurate financial picture.

Tax implications

- Tax regulations and period costs: According to IRS and HMRC guidelines, sales commissions are typically expensed in the period in which they are incurred. These regulations prevent commissions from being treated as product costs that would be capitalized. Unlike manufacturing costs that can be spread over time through depreciation, sales commissions are expensed immediately.

- Documentation and reporting: Proper record-keeping is essential for tax reporting. Accurate documentation of sales commissions helps ensure tax compliance and supports audit requirements. Misclassifying commissions could result in incorrect tax filings, potentially affecting deductions or causing penalties.

Decision-making implications

- Influence on strategic decisions: Recognizing sales commissions as period costs is crucial for decision-making. This accurate classification allows for better budgeting and forecasting, as businesses can predict costs tied to sales performance. It also ensures better financial planning and cash flow management, as commissions impact profitability in the period they are incurred.

- Performance evaluation: By treating commissions as period costs, companies can better evaluate sales team performance. This classification ensures expenses align with the revenue generated, offering a clear measure of the effectiveness of the salesforce.

Exceptions when sales commissions do not qualify as period costs.

Sales commissions are generally classified as period costs. However, there are circumstances where this classification may not apply. For instance, when commissions are recognized as income rather than expenses, they do not meet the definition of period costs. This occurs when a business earns commissions through sales partnerships. In such cases, these commissions are considered revenue and should be reported as such on the financial statements.

Additionally, the classification of sales commissions may depend on the structure of the commission incentives. According to ASC 606 regulations, companies must evaluate whether these costs are incremental to obtaining a customer contract. If the cost is incurred regardless of whether the contract is secured, it may not fit the period cost definition.

Key considerations:

- Exceptions primarily arise in businesses where commissions are recognized as income, requiring careful reporting

- Monthly, bi-monthly, quarterly, or annual payments may affect the assessment of period costs

- Industry norms usually favor classifying sales commissions as period costs to avoid compliance issues

Why understanding period costs matters for your bottom line

Understanding how to categorize expenses like sales commissions under period and product costs is essential for accurate financial reporting and effective cash flow management. Proper classification not only influences your income statement but also impacts decision-making, profitability, and regulatory compliance.

As businesses strive for financial clarity, relying on sales commission software can simplify capitalizing, forecasting, and reporting of sales commissions, offering accurate insights while maintaining compliance.

Frequently Asked Questions

.avif)

.avif)

.avif)