As explained in SaaS revenue recognition with ASC 606, for businesses based on recurring revenue, complying with the new accounting principle ASC 606 (IFRS 15) means recognizing revenue from customer contracts along with the costs incurred to obtain and fulfill them. (for example, a sales commission).

But all of this seems easier said than done, right? So, how do you actually crack the revenue recognition standard in your SaaS company’s financial reporting process and apply it to your sales commissions?

Well, you’ll get them answered as we walk you through the specific accounting changes that every SaaS company should stick to while preparing their financial statements for their sales commissions. Let’s dive in!

Understanding Sales Commissions Expense with Subtopic ASC 340-40

When ASC 606 (IFRS 15) was being rolled out by FASB (Financial Accounting Standards Board) and IASB (International Accounting Standards Board), they also introduced a separate set of guidance (ASC 340-40: Other Assets and Deferred Costs) on how companies should account for commission expenses associated with their customer contracts. This was added as a sub-topic under the existing ASC 340 revenue recognition standard.

ASC 340-40 covers amortization of assets arising from costs to obtain or fulfill a contract, and impairment of assets arising from those costs. This implies that businesses must now capitalize commission costs and amortize those costs over a period of time (i.e) the life of the sales contract to match the timing of the revenue – a complicated, high-stakes task.

This sounds scary for SaaS companies because the sales commission impact is often more significant and requires a substantial amount of work than the revenue impact.

The Impact of ASC 606 and ASC 340-40 on SaaS Sales Commissions

With regards to sales compensation, ASC 606 requires finance to amortize commission expense for individual sales reps over the length of contracts.

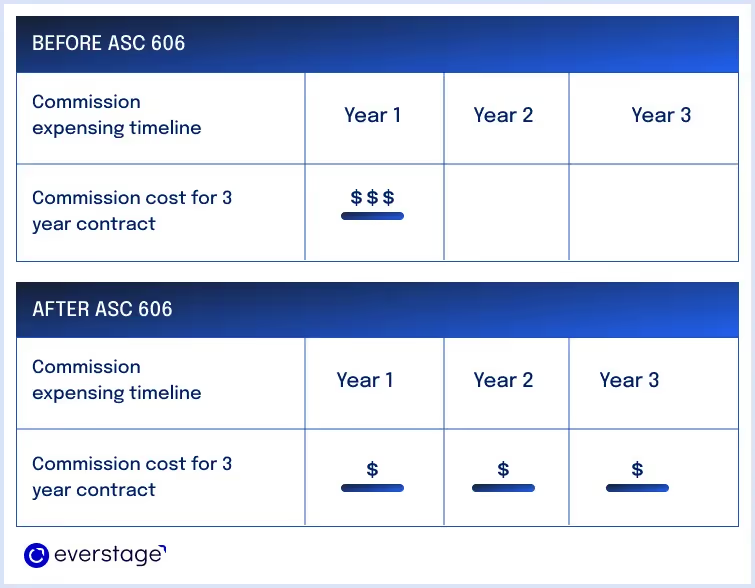

Let’s take an example. Before ASC 606, if your sales rep sold a three-year contract and was paid $150,000 in commission, you’d be recognizing the entire $150,000 expense in the same year in which the three-year deal was sold.

But, after ASC 606, you’d have to capitalize the $150,000 and amortize it over the three-year period of the contract.

Simply put, you’d have to recognize your sales incentives over the period of service depending upon the customer contract and estimated lifetime. This completely alters the way you recognize commission expenses which is one of the biggest portions of CAC for your SaaS business.

Note: ASC 606 will NOT change the structure of sales compensation plans.

Treatment of SaaS Commission Costs under ASC 606 and ASC 340-40

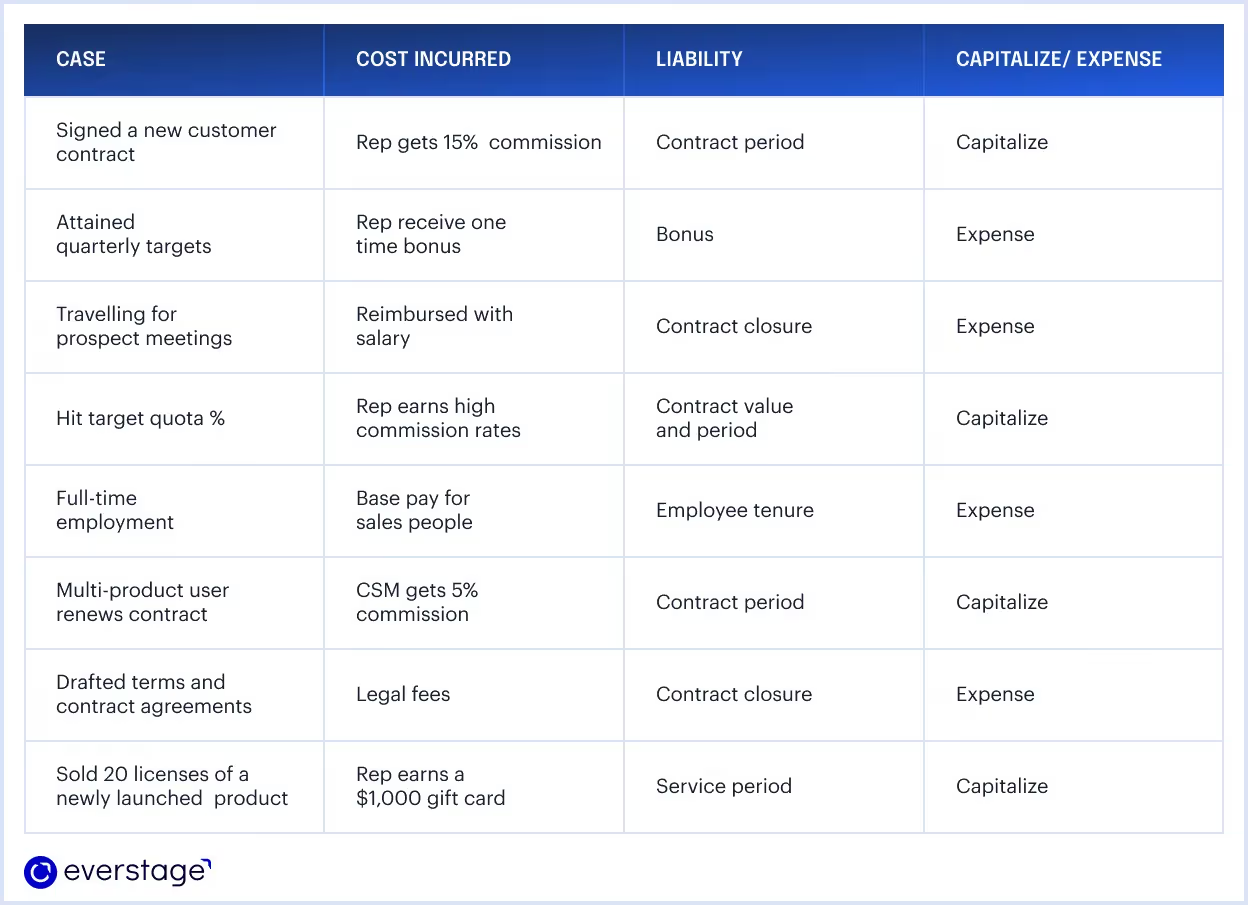

The adoption of ASC 606 and ASC 340-40 in your accounting activities starts with identifying the costs that can be accounted for when incurred and which ones need to be capitalized.

Generally, the below-mentioned costs can be capitalized and amortized:

- Sales commissions

- One-time SPIFs/bonuses related to sales

- Fringe benefits related to the sales commission, SPIF, and bonus payouts

To provide you with a better understanding of the treatment of various incremental costs like your sales commissions, we’ve listed a few cases along with a simplified decision-making workflow.

By now, you’d have acknowledged the necessary sales commission expense accounting changes based on the new revenue recognition standard: ASC 606. And, the million-dollar question for you would be: What exactly needs to be done to ensure that your sales commission plans are ASC 606 audit-ready?

Guess what? We’ve got you covered there as well.