TL;DR

SaaS revenue recognition with ASC 606 ensures accurate financial reporting by recognizing revenue as services are delivered, not when payments are received, and changes how commissions are accounted for.

- Understand the challenges unique to SaaS revenue recognition and why traditional models fall short.

- Learn how ASC 606’s five-step framework addresses complex contracts and variable pricing.

- See how commission expenses shift to capitalization and amortization, impacting expense timing.

- Gain clarity on compliance, transparency, and comparability in SaaS financial reporting.

You should be reading this if:

- You’re in the financial reporting space and want to understand revenue recognition thoroughly

- You’ve just heard of the term ‘ASC 606’ and are looking to find out if it will affect your SaaS company

- You’re generally curious to know what’s causing the hype around the new compliance.

Whatever be the case, you’re in the right place. We’ve paraphrased information on all things ASC 606 to shed some light on the new scheme of accounting for the revenue of your SaaS business.

In the first of the three-part ASC 606 blog series, we would be covering the ground from scratch. In square one, we’ll discuss what revenue recognition in SaaS means, its setbacks, and the rise of the new revenue recognition standard: ASC 606.

The State of Revenue Recognition in SaaS

If you’re in a traditional business model, the revenue recognition process is pretty straightforward. Your customer makes a one-time payment for your product or service, and then you provide the necessary product or fulfill the service at a specific date or time frame. You have clear data on when you exchange deliverables for the payment done by your customer. So, once the transaction is complete, you’re able to recognize the revenue immediately.

But, in SaaS, revenue recognition is tricky. Since the customers pay upfront for a product or service that is delivered over months or even years, the revenue can be recognized only as and when the customer contract progresses.

And as per GAAP (Generally Accepted Accounting Principles), the basic idea behind revenue recognition is that “bookings” shouldn’t be considered as “revenue” until you’ve delivered the service or product for which your customer has paid.

However, the status quo in SaaS behaves differently due to the prevailing gaps in accounting for revenue from customer contracts. How though?

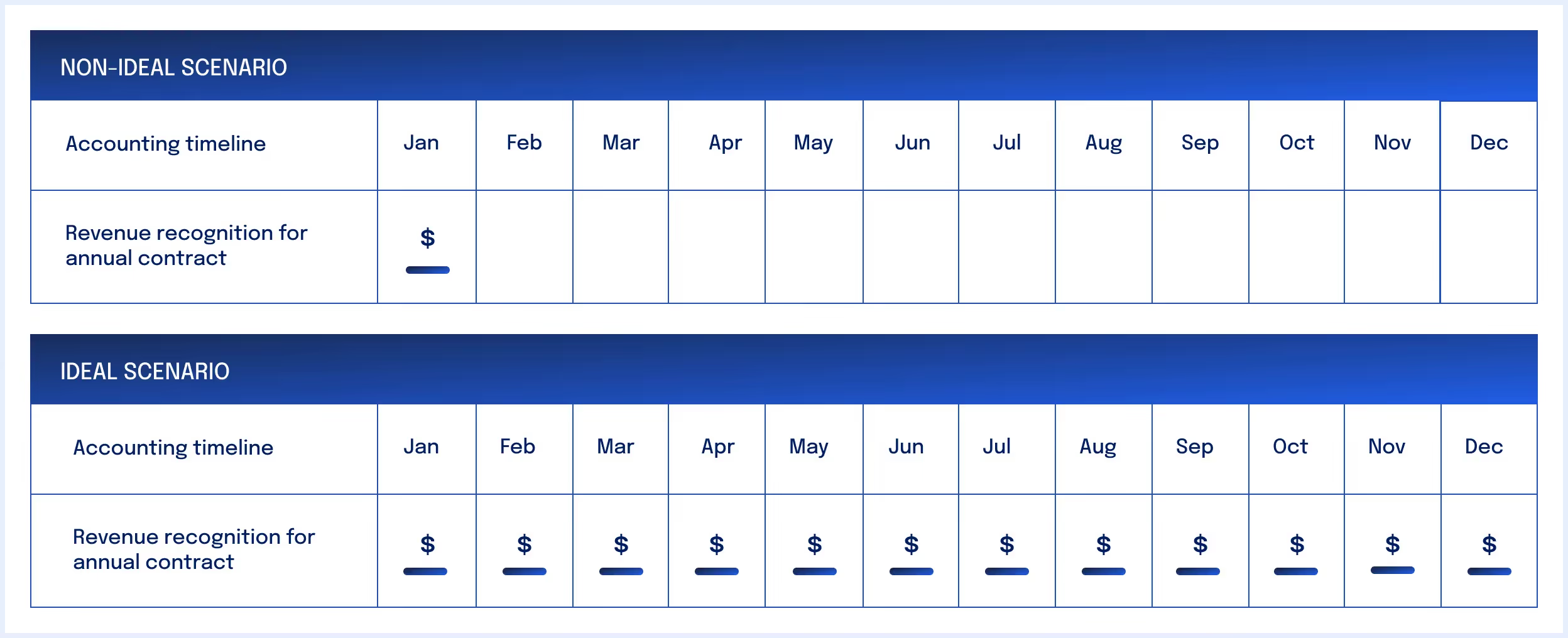

Consider the example below,

Your sales rep signed an annual plan for your product with a new customer for $32,000. Following the SaaS model, you’d be receiving the entire amount upfront from your customer at the time of annual subscription. You’re accounting for $32,000 as a part of your revenue immediately. But, according to GAAP, is this an ideal way to do it?

Definitely not, as you’d have received $32,000 in your account, but you haven’t earned the money yet as your service or product deliverables are ongoing and not fulfilled. So you shouldn’t be recognizing $32,000 as revenue in one shot. Instead, you should recognize $2,600 of revenue each month until the customer contract expires.

However, there were no guiding principles on recognizing revenue over the period of service and customer lifetime that was established by the board. So, SaaS companies continued reporting like the above-mentioned example for a long time. Also, recognizing revenue in the traditional way is not as simple as it sounds for a SaaS business. Let’s double down to understand the reasons behind it.

The Key Challenges in SaaS Revenue Recognition

The intricacies involved in SaaS subscriptions make it difficult to clearly define and apply accounting rules for sales taxes, contract renewals, commissions, and other variables. SaaS accounting could get even more complicated during,

Goes without saying, every SaaS business is unique from another. So, revenue recognition becomes convoluted as every company offers different subscription plans and pricing models based on the number of users, the volume of resources consumed, and the type of product/service being sold.

Getting revenue recognition right is critical for any business. With revenue being the fundamental financial metric used by investors and prospects to assess the company’s performance, it also represents the value of its products.

So, something REALLY BIG had to happen to address the complexities in SaaS and streamline its accounting once and for all.

The Arrival of ASC 606 Revenue Recognition Standard

With the growing number of SaaS businesses, the best practices in accounting had to be revisited as there was a dire need for guidance on some grey regions of revenue recognition—contracts involving multiple products and services, treatment of costs related to customer contract, and accounting for contract modifications.

So, the financial boards took the matters into their own hands and called for the biggest change to the accounting standards in the last 100 years—ASC 606.

Overview: ASC 606 (IFRS 15) are customer contract revenue recognition standards that made their debuts during May 2014. These accounting principles were the outcome of convergence work between FASB‘s (Financial Accounting Standards Board) ASU 2014-09, Revenue from Contracts with Customers (Topic 606) and IASB‘s (International Accounting Standards Board) (IFRS) 15, Revenue from Contracts with Customers. Along with this, a subtopic 340-40 was created to set standards related to costs incurred to obtain and fulfill customer contracts.

Effective dates: The new revenue standard affects all existing contracts with customers as part of a private company or a public company. It was made effective for public companies beginning with annual reporting periods after December 15, 2017, and was effective for non-public companies with annual reporting periods after December 15, 2019. For some non-public companies who were yet to issue financial statements had a one-year extension for revenue recognition. The effective date for the respective companies will be for fiscal years beginning after December 15, 2021 and interim periods within fiscal years beginning after December 15, 2022.

The Goals of ASC 606

The overall purpose of introducing these standards was to make it easier for companies to get on the same page with their accounting and establish a clear outline to determine revenue calculations for filings and tax purposes. Below are its set of goals,

- To facilitate an industry-neutral revenue recognition model to increase financial statement comparability among companies and industries.

- To set the best way forward for businesses to perform revenue reporting, filings and forecasting more effectively and efficiently.

- To create comprehensive disclosures on how businesses should calculate and report revenue.

- To enable finance teams to connect the revenue dots between the beginning and end of the company’s accounting periods to land on accurate revenue figures.

And as a way to achieve the above-mentioned objectives, the board of CPAs came up with a revenue recognition framework that could be adopted by companies across the world.

The Revenue Recognition Framework of ASC 606

The main objective behind providing guidelines was to enable companies to gain more clarity on their actual revenue generation. So, ASC 606 defines a flexible and robust five-step model for revenue recognition. This model simplifies the preparation of financial statements for businesses by directing how much and when to recognize revenue.

1. Identify the Contract with a Customer

A contract is an agreement between two or more parties, with obligations and rights that can be enforced when needed. Here are the important terms of the contract.

- The agreement must have the approval of every party

- The parties involved must confirm that they’re committed to fulfilling the obligations

- The rights of each party are identifiable

- Identify the payment terms

- The contract can be commercially substantive

- It’s likely that the vendor will receive payment

2. Identify Performance Obligation in the Contract

In simple terms, the performance obligation is a promise that has been made to transfer the goods or services from a vendor to a customer. ASC 606 also defines what makes a service distinct from others as follows,

- The actual goods and services must benefit the customer

- The goods and services can be identified on their own and can be transferred independently.

3. Determine the Transaction Price

This is the price that the vendor is expected to receive from their customers after the transfer of all the goods and services as promised in the contract. The transaction price can be a fixed amount and other variables like price considerations, bonuses, rebates, penalties, etc.

4. Allocate the Transaction Price to the Performance Obligations in the Contract

In this step, you allocate the price to each component in the contract. The delivery of a product or service can be recurring in the SaaS business model. And so, the total amount can be split as the revenue for each performance obligation.

5. Recognize Revenue When or as the Entity Satisfies a Performance Obligation

Once you’ve fulfilled all your performance obligations, recognize the revenue. This can happen over a period of time or at once, depending on the nature of your contract.

So far, we’ve covered how ASC606 has streamlined the revenue reporting process for SaaS companies along with the others. Now, let’s explore the nuances of ASC 606 w.r.t sales commissions.

Rethinking SaaS Sales Commission Accounting with ASC 606

With ASC 606 coming into effect, accounting for your sales commissions could feel like moving mountains. You may ask: How exactly?

Well, considering the fact that ASC 606 takes into account the entire lifecycle of a customer and the contract costs incurred by them at every stage of the business,

It becomes essential to determine if your sales incentives need to be expensed or capitalized. For the commission costs that require to be capitalized, you’d have to recognize them over the period of service depending upon the customer contract and estimated lifetime.

Also, the most significant impact of ASC 606 relates to the timing of revenue recognition. So, this will have an exponential effect on compensation calculations linked to revenue, such as sales commissions and bonuses.