TL;DR

- ASC 606 is the revenue recognition standard governing how SaaS businesses account for sales commission costs. It requires capitalization and amortization of incremental contract costs.

- A structured, seven-step approach helps SaaS finance teams achieve ASC 606 compliance, accurate reporting, and alignment with business goals.

- Reassess current commission structures and link incentives directly to company objectives.

- Categorize commission costs properly to produce audit-ready financial statements.

- The five-step revenue recognition model (identify contract, identify obligations, determine price, allocate price, recognize revenue) forms the foundation of ASC 606 compliance.

- Expert-backed steps and automation through platforms like Everstage make ASC 606 adoption manageable and audit-ready for SaaS CFOs and Controllers.

What Is ASC 606?

ASC 606 is the accounting standard that governs how companies recognize revenue from customer contracts. It requires businesses to record revenue when control of goods or services transfers to the customer, based on the amount they expect to receive. The standard provides a consistent, principles-based framework across industries, including SaaS.

ASC 606 Definition

ASC 606 (Revenue from Contracts with Customers) is the FASB-issued accounting standard establishing a unified framework for recognizing revenue. ASC 606 replaced legacy, industry-specific guidance with a single, principles-based model applicable to all industries, including SaaS and technology companies.

ASC 606 requires companies to recognize revenue when control of goods or services transfers to the customer. The recognized amount reflects the consideration the company expects to receive. SaaS businesses feel a direct impact on how sales commissions are expensed. Commissions paid to acquire customer contracts qualify as incremental costs requiring capitalization and amortization over the expected benefit period instead of expensing immediately.

SaaS CFOs, Controllers, and finance leaders need to ensure their commission plans remain compliant, audit-ready, and accurately reflected in financial statements.

The Five-Step Revenue Recognition Model

Contract identification and performance obligation mapping form the backbone of ASC 606's five-step model. Grasping these steps is critical before applying ASC 606 to your sales commission plans.

The five-step ASC 606 revenue recognition model with corresponding sales commission considerations for each step.

Every decision in your ASC 606 implementation, from categorizing costs to determining amortization periods, flows from this model.

Previous installments in our ASC 606 series covered SaaS revenue recognition with ASC 606 and its impact on SaaS sales commissions. Early adopters confirm that the transition demands significant time and specialized expertise. If you are still aligning your sales commission plans with ASC 606 (IFRS 15), simplify your compliance process with the expert-backed steps below.

Learnings from finance leaders who have completed the commission expense recognition transition will help you find a straightforward, effective adoption path.

In part three of our ASC 606 series, we summarize the essential steps SaaS companies need to implement ASC 606 and produce audit-ready sales commission plans, based on conversations with SaaS CFOs and Controllers.

Here is each step, designed for a confident ASC 606 implementation.

Step-by-Step Guide to ASC 606 Implementation in Your Sales Commission Plans

Reassessing commission types and producing audit-ready reports are the bookends of a structured ASC 606 implementation. The following guide walks SaaS finance teams through every critical phase, connecting each step to the broader five-step revenue recognition model.

1. Re-examine Your Type of Sales Commissions

Collecting historical commission data and mapping each incentive to a business goal are the first priorities in this step. Review the types of commissions you currently offer to your sales reps and how their payments are calculated. Identify the purpose of every incentive and align it against your business objectives.

With this data, you can grasp the existing state of commissions in your organization. Use it to analyze all components of your variable compensation plan. Confirm your top management and sales teams are aligned on the plan structure.

A complete view of your variable compensation data and existing commission plan types is critical for producing ASC 606-compliant financial reports. SaaS CFOs and Controllers face added complexity here because subscription-based models involve multi-year contracts and renewal deals, each with different ASC 606 treatment requirements.

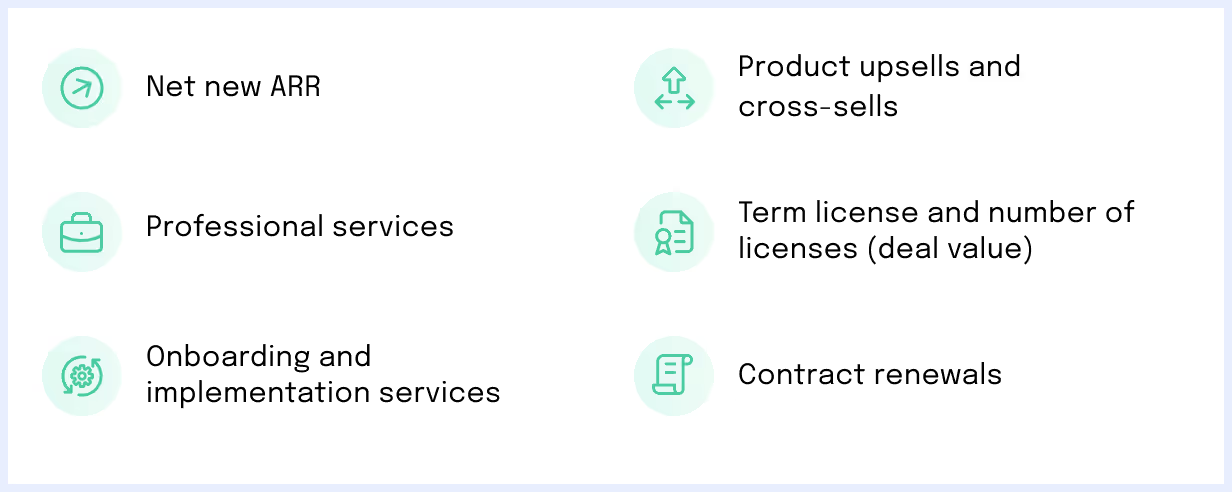

2. Categorize Your Reps' Commissions Based on Customer Benefits

Linking commission components to the benefit or service provided to customers is the core task in this step. You may have multiple commission components driving reps toward a specific sales goal or behavior. Some of those components tie directly to the benefit or service delivered to your customers. The commissionable component may carry a different time to value from your customers' perspective.

Below are sales commission costs which associate with customer benefits:

Check your historical data and classify your commission costs according to their linkage with the services included in the initial contract. Doing so lets you identify the cases where contract costs need to be capitalized.

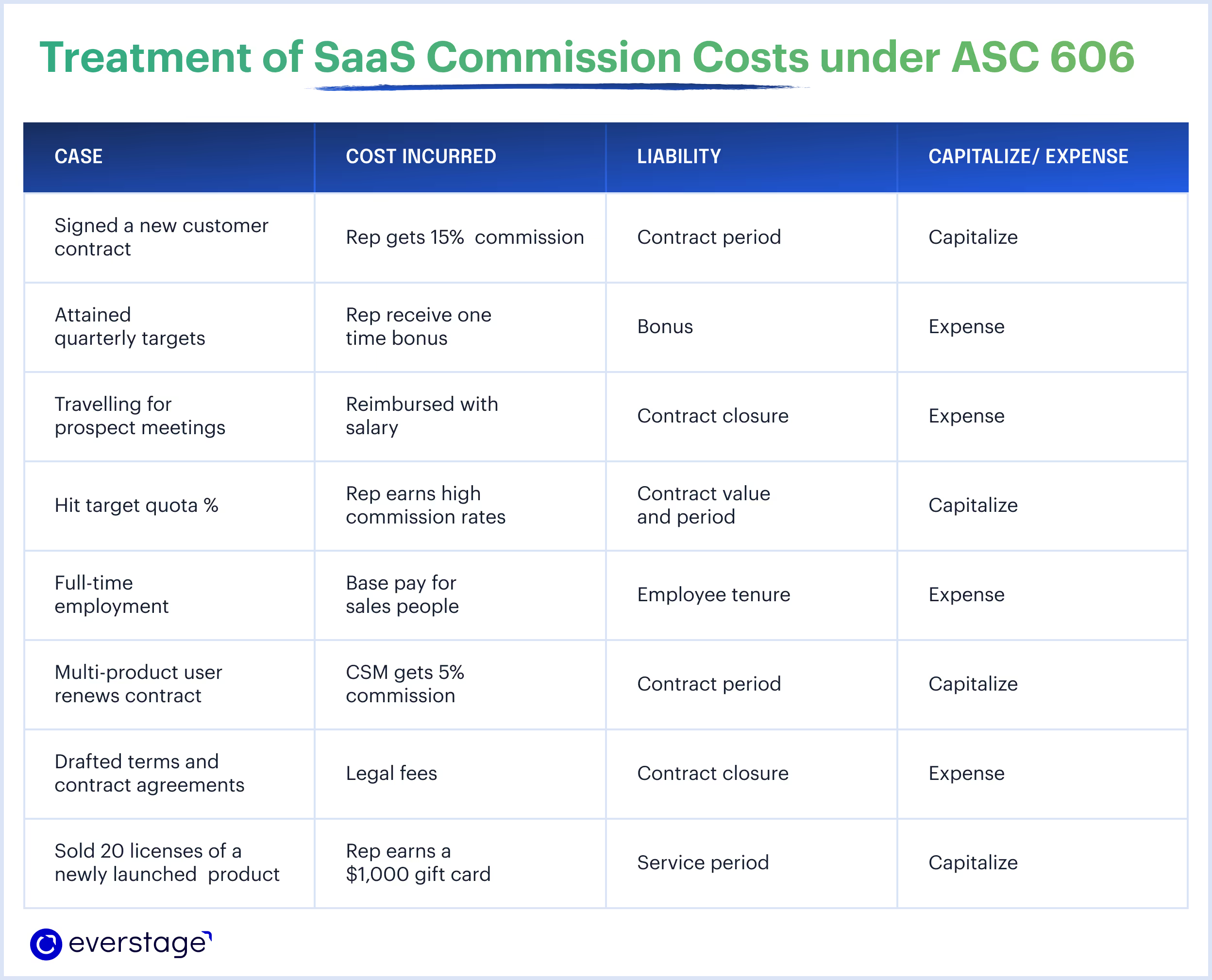

3. Identify Your Treatment for Various Commission Costs

FASB's ASC 340-40 defines incremental costs as costs that an entity incurs to obtain a contract with a customer (for example, a sales commission).

Separating costs which can be expensed when incurred from those requiring capitalization is the central task here. If the commission is capitalizable, you should capitalize at the point of accrual. Refer to the table below for the treatment of commission costs across specific sales use cases.

4. Evaluate Your Amortization Period for Incremental Costs

Estimating the long-term benefit of each commission payment and identifying the inputs behind the benefit are the two priorities in this step. Assign a typical amortization period based on the contract term and estimated customer lifetime (how long you expect to do business with a customer beyond the contract term).

In the SaaS model, some inputs are obvious: the initial contract term and expected renewals extending the customer lifetime. A less obvious input is technology life.

Consider a customer who purchased your product three years ago. Your product may have matured or become outdated over this period. Either way, the commission paid on the initial contract loses relevance, and the amortization period would be limited to about three years. Due to this shift, your input for estimating the amortization period could be affected.

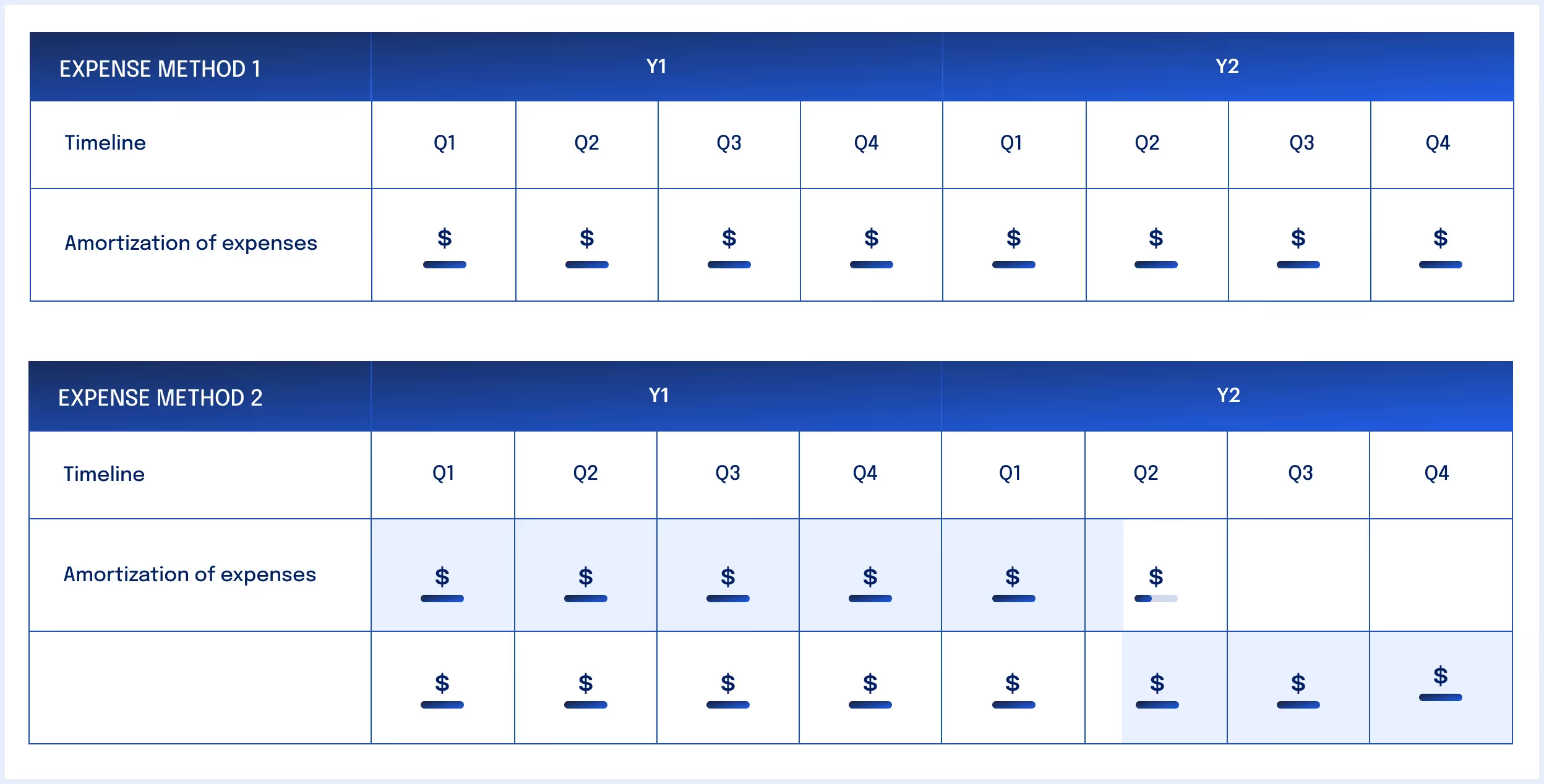

5. Determine Your Amortization Method

Even amortization is one option, but it is not the only one. With a 24-month amortization period, you could expense 1/24th each month.

You can also choose to expense 2/3 the first year and 1/3 the second. Ensure you have a documented rationale that justifies your chosen amortization methodology.

Portfolio expensing offers another approach. You can account for multiple contracts as a portfolio if certain ASC 606 criteria are met. Under this method, identify customer segments and amortize them over the estimated lifetime of the segment. You can also group commissions by product type or region and assign an amortization life for each group.

Portfolio expensing requires a high sales volume to work well. If you close only a few large deals per quarter, too much variability in contracts and delivery periods makes this approach impractical.

6. Allocate Transaction Price and Discounts to Multiple Performance Obligations Within a Contract

On allocating transaction price: When your customer contract contains more than one performance obligation, ASC 606 (IFRS 15) requires you to allocate the transaction price based on relative stand-alone selling prices. The stand-alone selling price is the price at which you would sell a product or service separately to your customers at contract inception.

If this price is unavailable, estimate it using the adjusted market assessment approach or the expected cost plus margin approach. A residual approach is also permitted under specific circumstances.

On allocating discounts: ASC 606 and IFRS 15 specify that when a customer receives a discount for purchasing a bundle, you must allocate the discount based on relative standalone selling prices to all performance obligations, unless there is observable evidence that the discount relates to one or more (but not all) obligations. Deloitte's ASC 606 Revenue Roadmap and IFRS 15 Illustrative Examples 33 and 55–56 provide detailed guidance on allocating discounts to specific performance obligations.

IFRS 15 illustrative example (IE) 33 on the allocation methodology and IE 169-172 on allocating a discount to one or more performance obligations provide detailed guidance.

On allocation method: SaaS businesses may benefit from a specific allocation approach. If you can objectively determine if a contract cost asset applies to one or more distinctive services in your customer contract (and not all), allocating the contract cost asset entirely to that service(s) may be reasonable. Under ASC 340-40, these costs are recognized as assets (costs to fulfill a contract) because they relate primarily to activities fulfilling the contract without transferring a product or service to the customer.

An example: paying a specific commission amount for selling a product that differs from the commission amount for performing professional services.

7. Perform Detailed Data Reporting and Accurate Calculations

Disaggregating commission data to the contract or product level and maintaining audit-ready calculations are the two critical tasks in this final step. Before ASC 606, most companies performed sales commission calculations with aggregated sales data based on the company's monthly ARR.

ASC 606 requires companies to disaggregate their data to show multiple products with differing revenue patterns, such as up-front fees and post-contract services. Slicing commission calculations to the contract or product level, or applying a reasonable estimation method, is essential. You can then use the data for financial statements and ongoing compliance analysis.

You must have the data at your fingertips to perform math on sales basis, cash, accrual, and deferred revenue, with accounting methods chosen on a case-by-case basis.

Reconciling commission data across CRM, ERP, and payroll systems is a frequent challenge at this stage. Maintaining data integrity during manual transfers compounds the risk. Automating commission calculations with a purpose-built platform like Everstage eliminates these risks and ensures real-time accuracy.

P.S. You must successfully complete all 7 steps for every single customer contract in your business to achieve ASC 606 compliance.

Common ASC 606 Implementation Challenges

Fragmented data systems and cross-departmental misalignment are two of the most frequent obstacles SaaS finance teams face during ASC 606 implementation. Anticipating these challenges helps you plan effectively and avoid costly delays.

- Data collection and integration: Commission data lives across CRM, ERP, and payroll systems, making contract-level consolidation difficult.

- Cross-departmental alignment: Sales, finance, and legal teams must agree on contract terms and commission structures. Misalignment leads to reporting errors.

- Determining amortization periods: Estimating customer lifetime and technology life requires judgment calls auditors will scrutinize.

- Handling contract modifications: Renewals and upsells trigger re-evaluation of capitalized costs and amortization schedules.

- Manual spreadsheet limitations: Excel-based processes break down at scale, introducing errors and making audit trails nearly impossible to maintain.

- Keeping up with updated guidance: FASB periodically issues updates and clarifications affecting your implementation approach.

Investing in automation, establishing clear cross-functional workflows, and documenting every assumption for audit readiness are the most effective ways to overcome these challenges.

Summary of ASC 606 Implementation

ASC 606 implementation in sales commission plans requires extensive time, specialized expertise, and cross-functional coordination. Managing this process in Excel creates a significant burden for finance teams. The volume of contract-level data and amortization schedules makes manual approaches unsustainable at scale.

Sourcing and cross-verifying data from multiple applications manually is exhausting and error-prone, especially without a clear view of historical data.

Staying ASC 606 compliant should be straightforward and stress-free. Automating your sales commission calculations and reporting with an ASC 606-compliant platform like Everstage is the most effective path to achieve the goal.

Everstage is the only ASC 606 compliance platform purpose-built for SaaS, offering the fastest implementation, granular real-time reporting, and dynamic true-up entries. It provides all the data SaaS CFOs and Controllers need to meet revenue recognition standards:

- Historical commission data

- Customizable reports and dashboards

- LTD Cost Waterfall

- Deferred costs

- Amortization period and amounts

- Detailed period rolls

- Dynamic true-up entries

Why Everstage?

- Fastest time-to-value for ASC 606 compliance

- Purpose-built for SaaS sales commissions

- Real-time, audit-ready reporting

- Dynamic true-up entries unique to Everstage

- Top-rated support and onboarding

Book a Demo: See ASC 606 Automation in Action